Searching for a 100000 naira loan without BVN in Nigeria? Let’s start with brutal honesty, because you deserve the truth before chasing impossible promises about getting 100000 to 500000 naira loan without BVN.

If someone tells you they can get you a 100000 naira loan without BVN, without collateral, without guarantors, and without any meaningful verification… they’re either lying, running a scam, or offering terms so predatory that you’ll regret ever borrowing. The same applies to those promising 200000 naira loan without BVN or 500000 naira loan without BVN with zero verification.

- Why 100000 Naira Loan Without BVN Are Nearly Impossible

- Alternative Verification Methods for 100000 Naira Loan Without BVN

- The Hybrid Strategy: Building Up to 100000 Naira Loan Without BVN

- Why Most “₦500,000 Without BVN” Claims Are Scams

- Realistic Expectations for 100000 to 500000 Naira Loan Without BVN

- Safer Alternatives to 100000 Naira Loan Without BVN

- Red Flags and Warning Signs

- Building Your Financial Profile for Future Access

- Frequently Asked Questions

- Key Takeaways: Making Smart Decisions

I know that’s not what you wanted to hear. Maybe you’re in a tight spot… business capital needed urgently, school fees deadline approaching, family emergency that can’t wait. You’ve seen those ads: “Get ₦500,000 instantly, no BVN required!” It sounds perfect.

But here’s what those ads don’t tell you: large loans without verification either don’t exist, come from illegal lenders who’ll make your life hell, or have so many hidden catches that “no BVN” is technically true but practically meaningless.

Does this mean you’re out of options? Absolutely not. There are legitimate ways to access ₦100,000 to ₦500,000 loans when BVN is a concern. But they all involve trade-offs: alternative verification, collateral, guarantors, or eventually providing BVN after proving yourself with smaller amounts.

This guide will walk you through realistic, safe options for accessing larger loans when traditional BVN verification isn’t ideal. No fairy tales. No false promises. Just practical strategies that actually work in Nigeria’s financial reality.

Why 100000 Naira Loan Without BVN Are Nearly Impossible

Before exploring solutions for getting 100000 naira loan without BVN, let’s understand why loans without BVN become exponentially harder as amounts increase from 10000 naira to 100000 naira loan without BVN or even 500000 naira.

Think about it from a lender’s perspective. If someone wants to borrow a small 10000 naira loan without BVN, the risk is manageable. Even if they default, the loss is relatively small. Lenders can absorb occasional defaults, factor them into interest rates, and still profit.

But a 100000 naira loan without BVN or 500000 naira loan without BVN? That’s a different game entirely. If someone borrows ₦500,000 and disappears, the lender takes a massive hit. Without BVN verification, the lender has limited recourse. They can’t track you across banks, can’t report you to credit bureaus effectively, can’t easily recover the funds.

This is why legitimate lenders follow a simple rule: The larger the loan, the stronger the verification required.

For ₦10,000 loans without BVN, apps use phone data, contacts, and transaction history. It’s not ideal verification, but it’s enough for small amounts.

For 100000 naira loan without BVN or larger amounts like 200000 to 500000 naira? No reputable lender relies on phone data alone. They need something more substantial:

Bank Verification Number (BVN) linking all your accounts and credit history. Physical collateral (property, vehicles, equipment) they can claim if you default. Personal guarantors with verified income who’ll repay if you don’t. Employment verification with salary earmark (direct deduction from your paycheck). Business documentation proving revenue and assets for business loans.

Lenders operating without ANY of these safeguards on large loans are either:

Scammers who’ll take upfront fees and disappear. Illegal operators who’ll use harassment, threats, and violence for collection. Predatory lenders charging 50-100% monthly interest rates that trap you in debt. Fronts for fraud using your information for identity theft and financial crimes.

This reality check isn’t meant to discourage you. It’s meant to protect you from making decisions that could destroy your financial life for years.

Now let’s explore what actually works.

Alternative Verification Methods for 100000 Naira Loan Without BVN

If you need a 100000 naira loan without BVN or even larger amounts like 200000 to 500000 naira, legitimate lenders offer alternative verification methods. According to Credit Nigeria’s loan guidelines, these aren’t “loopholes” – they’re official processes designed to assess creditworthiness through different means while respecting privacy concerns.

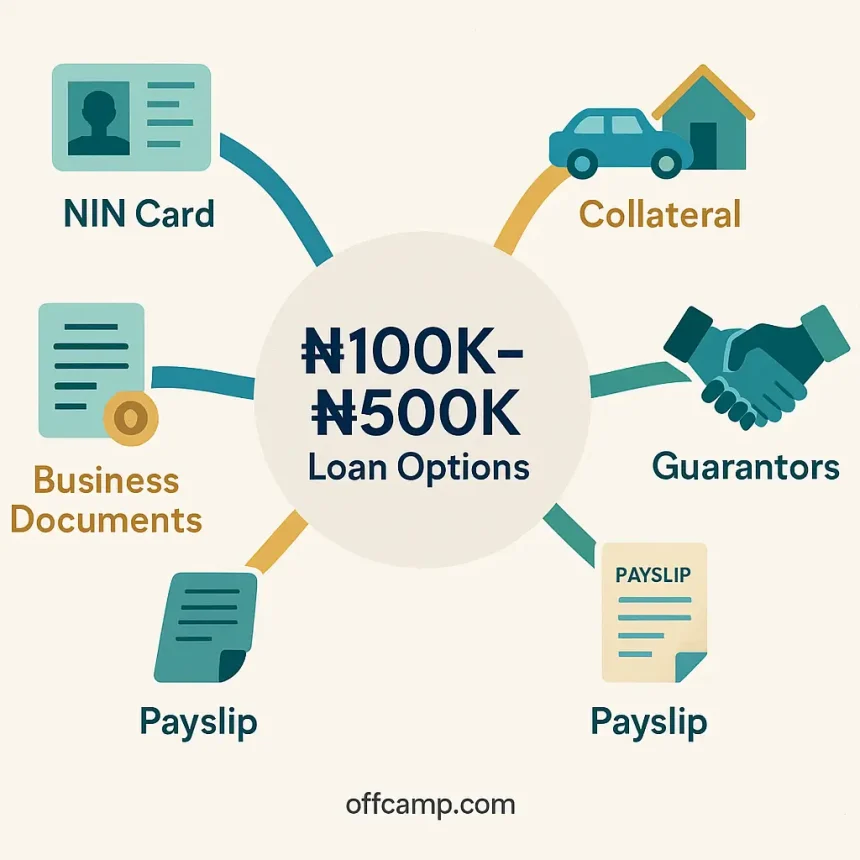

1. National Identity Number (NIN) Verification

Nigeria’s National Identity Management Commission (NIMC) issues National Identity Numbers that serve similar functions to BVN but aren’t directly linked to your banking activity.

Some loan apps accept NIN as primary verification for loans up to ₦100,000 to ₦200,000. The NIN confirms your identity, address, and biometric data without exposing your complete financial history.

How it works: You provide your 11-digit NIN during application. The lender verifies your identity through NIMC database. They assess creditworthiness using phone data, transaction history from SMS, and other behavioral indicators. Loan approval happens without accessing your BVN-linked bank information.

Realistic expectations: NIN verification typically caps at ₦100,000 to ₦200,000 for first-time borrowers. Interest rates are higher than BVN-verified loans (18-30% monthly versus 5-15%). You’ll still need to grant extensive phone data access. For amounts above ₦200,000, most lenders eventually require BVN anyway.

Best apps for NIN verification:

QuickCheck: Accepts NIN for loans up to ₦150,000 initially. Carbon: Will consider NIN combined with strong transaction history for up to ₦100,000. FairMoney: Offers NIN pathway for first loans under ₦150,000.

2. Collateral-Based Loans: The Most Reliable Path for 100000 Naira Loan Without BVN

This is the most reliable way to access 100000 naira loan without BVN or even 200000 to 500000 naira without BVN verification. When you provide physical collateral through Nigeria’s National Collateral Registry, lenders care less about your BVN because they have tangible security.

Acceptable collateral in Nigeria:

Real estate: Land titles, building ownership documents. Vehicles: Car registration papers (Lagos and FCT particularly accept this). Equipment: Business machinery, generators, industrial tools. Electronics: High-value items (laptops, phones, cameras) at pawn shops or collateral lenders. Jewelry: Gold, silver, valuable pieces at specialized lenders. Certificates of Deposit: Fixed deposit receipts from banks. Business inventory: Stock, goods, raw materials for business owners.

How collateral loans work:

Visit a microfinance bank, credit union, or specialized collateral lender (not apps). Bring documentation proving ownership of the collateral. The lender appraises the collateral (usually 50-70% of actual value). You receive a loan based on collateral value, not BVN. Interest rates are lower than unsecured loans (typically 5-15% monthly). If you default, the lender claims the collateral, not your bank accounts.

Recommended collateral lenders:

AB Microfinance Bank: Offers ₦15,000 to ₦5,000,000 with collateral, minimal BVN reliance. LAPO Microfinance Bank: Accepts various collateral types, serves rural and urban areas. Local credit unions: Often more flexible about BVN if you provide strong collateral. Pawn shops: For quick ₦50,000 to ₦300,000 on valuable items.

3. Guarantor-Based Loans

In Nigerian financial culture, guarantors carry significant weight. If credible guarantors with verified income vouch for you, some lenders will reduce or eliminate BVN requirements.

What makes a good guarantor:

Must have BVN and good credit history (the irony, right?). Employed with consistent salary or proven business income. Willing to sign legal documents accepting repayment responsibility. Preferably has existing relationship with the lender. Ideally, a family member or very close friend (not just acquaintances).

How it works:

You apply for a loan explaining why you can’t provide BVN. You present one or more guarantors (larger loans need 2-3 guarantors). The lender verifies the guarantors’ income, employment, and creditworthiness. Loan approval is based on guarantor strength, not your BVN. If you default, the lender pursues the guarantors, not you directly.

Where to get guarantor-based loans:

Cooperative societies: Very common in Nigeria, often don’t require borrower’s BVN if guarantors are strong. Microfinance banks: Many accept guarantor-based lending, especially in communities where they operate. Credit unions: Traditional guarantor systems, often more flexible than commercial banks. Employer-based schemes: Some companies offer staff loans with colleague guarantors, minimal BVN checks.

Real talk: Finding guarantors willing to take on ₦100,000 to ₦500,000 liability is tough. Most people won’t risk their financial standing for someone else’s loan. But for family emergencies or business ventures with clear repayment plans, it’s possible.

4. Salary Earmark Loans

If you’re employed, salary earmark loans bypass traditional BVN verification by deducting repayment directly from your paycheck before you receive it.

How salary earmark works:

Your employer partners with a lender or microfinance bank. You apply for a loan through your company’s arrangement. The lender verifies your employment and salary level directly with HR. Loan approval is based on employment verification, not BVN. Monthly repayment is automatically deducted from your salary at source. Since repayment is guaranteed through salary deduction, BVN becomes less critical.

Realistic amounts:

Most salary earmark programs offer 1-3 months’ gross salary as loan amount. If you earn ₦150,000 monthly, you might access ₦150,000 to ₦450,000. Interest rates are typically lower than app-based loans (5-10% monthly). Repayment periods extend to 6-12 months depending on amount.

How to access:

Check if your employer has partnerships with lenders like Renmoney, Page Financials, or local microfinance banks. Request loan application through HR department. Complete employment verification forms. Receive funds without providing BVN, secured entirely through salary deduction.

Limitation: Only works if you’re formally employed with consistent payroll. Self-employed, freelancers, and informal sector workers won’t qualify.

5. Business Documentation Loans

For entrepreneurs and business owners, strong business documentation can sometimes substitute for BVN verification on larger loans.

Required business documentation:

CAC (Corporate Affairs Commission) registration certificate. Tax clearance or TIN (Tax Identification Number). Bank statements showing business transactions (yes, this requires a bank account, but not BVN exposure). Business licenses, permits, or registrations specific to your industry. Evidence of contracts, purchase orders, or steady customers. Business assets inventory or valuation.

How it works:

Approach business-focused lenders (not consumer loan apps). Present comprehensive business documentation. Lender assesses business viability and revenue potential. Loan approval is based on business strength, not personal BVN. Interest rates align with business loan standards (3-15% monthly). Repayment expectations tied to business cash flow.

Best sources:

Bank of Industry (BOI): Government institution offering business loans with flexible verification. NIRSAL Microfinance Bank: Focuses on SMEs, agribusiness, less rigid on personal BVN. Tony Elumelu Foundation: Offers grants and loans for startups, minimal BVN focus. Business development programs: Various government and NGO programs supporting entrepreneurs.

Reality check: Accessing ₦100,000+ through business channels requires legitimate, documented business operations. You can’t just claim you have a business; you need proof of revenue, operations, and viability.

The Hybrid Strategy: Building Up to 100000 Naira Loan Without BVN

Here’s a smarter approach many successful borrowers use to eventually access 100000 naira loan without BVN or larger amounts: start small, build credit, access larger amounts progressively while minimizing BVN exposure.

Step 1: Start with Small No-BVN Loans (₦10,000-₦20,000)

Use apps like PalmCredit, KashNow, or GoCash that offer initial loans without BVN. Borrow small amounts (₦10,000 to ₦20,000). Repay perfectly on time or early. Your internal credit score with these apps skyrockets.

Step 2: Graduate to Medium Loans (₦50,000-₦100,000)

After 2-3 successful small loans, apps offer higher limits. Some still don’t require BVN at this level, using your repayment history as primary credential. Borrow ₦50,000 to ₦100,000, continue perfect repayment. You’re building verifiable credit history without full BVN exposure.

Step 3: Provide BVN Strategically for Large Amounts

Now you have options. Either continue with the same apps (who know you’re reliable) and provide BVN to unlock ₦200,000 to ₦500,000 at better rates. Or approach new lenders with your documented repayment history from previous apps as proof of creditworthiness.

Why this works:

You’ve proven reliability through behavior, not just paperwork. Your repayment history is valuable currency that reduces lender risk. When you eventually provide BVN (if you choose to), you’re negotiating from strength, not desperation. You’ve built credit score and reputation that command better terms.

Timeline: This strategy takes 6-12 months of consistent borrowing and repayment. But it’s infinitely safer than chasing “instant ₦500,000 no BVN” scams.

For those considering this path, understanding the full spectrum of loan options helps you plan the progression strategically.

Why Most “₦500,000 Without BVN” Claims Are Scams

Let’s talk about those tempting ads and WhatsApp messages promising huge loans without verification.

Common scam patterns:

“Join our WhatsApp group for instant ₦500,000 loan, no BVN!” – Then they demand “processing fees” upfront. Once you pay, they disappear or demand more fees.

“We have special CBN-approved scheme for BVN-free loans up to ₦1 million!” – There’s no such scheme. They’re using official-sounding language to seem legitimate. Eventually they’ll request fees, personal information for identity theft, or “collateral” that’s really just stealing from you.

“Foreign investors offering Nigerian loans without local verification” – Classic advance fee fraud. They’ll string you along with forms, applications, and promises while extracting money at each step.

“Government grant program disguised as loans, no BVN required!” – Real government programs (like BOI loans or Tony Elumelu grants) have official websites and processes. These scammers create fake sites that look official.

“Peer-to-peer lending platform connecting you with private lenders” – Sounds modern and tech-savvy. Reality: fake profiles, fake “lenders,” real fees you’ll never recover.

Red flags to watch for:

Requesting any upfront payment before loan disbursement (processing fees, insurance, registration, etc.). No physical office address or website, only WhatsApp/Telegram contact. Promises that sound too good to be true (“₦500,000 in 5 minutes, no questions asked”). Pressure tactics (“This offer expires today, act now!”). Poor grammar, spelling errors, unprofessional communication. Asking for unusual information (ATM PIN, OTP codes, full card details).

What actually happens to scam victims:

You lose the “processing fee” (usually ₦5,000 to ₦50,000). Your personal information gets sold to other scammers. Your bank details might be used for fraud attempts. You waste time and emotional energy on false hope. You become desperate and vulnerable to even worse scams.

According to Credit Nigeria, legitimate lenders follow Central Bank of Nigeria regulations requiring identity verification for loans above certain thresholds. Claims of completely unverified large loans violate these regulations, which means they’re either illegal or fictitious.

Realistic Expectations for 100000 to 500000 Naira Loan Without BVN

Let’s break down what’s actually achievable for getting 100000 naira loan without BVN or larger amounts at different levels without full BVN verification.

100000 Naira Loan Without BVN Requirements

Most realistic path: NIN verification + strong phone data + small collateral or one guarantor.

Expected interest rate: 15-25% monthly

Typical approval time: 1-7 days (longer than small loans due to verification requirements)

Repayment period: 30-90 days

Success factors:

- Proven income through bank transaction SMS

- Clean borrowing history if you’ve used loan apps before

- Stable employment or business documentation

- Willingness to provide extensive phone data access

Apps/lenders that might approve:

- QuickCheck (with NIN)

- Carbon (after building history with smaller loans)

- FairMoney (NIN + transaction history)

- Local microfinance banks (with collateral or guarantor)

200000 Naira Loan Without BVN Expectations

Most realistic path: Collateral + NIN or guarantor + employment verification for 200000 naira loan without BVN.

Expected interest rate: 10-20% monthly

Typical approval time: 3-14 days

Repayment period: 60-180 days

Success factors:

- Tangible collateral worth ₦300,000+ (they lend 50-70% of value)

- Strong guarantor with proven income

- Documented employment with ₦100,000+ monthly salary

- Established business with verifiable revenue

Lenders to approach:

- Microfinance banks in your area

- Credit unions or cooperative societies

- Employer-backed loan programs

- Asset-based lenders (for collateral loans)

500000 Naira Loan Without BVN Reality Check

Most realistic path: Strong collateral + business documentation or formal employment with salary earmark for 500000 naira loan without BVN.

Expected interest rate: 5-15% monthly (lower because collateral reduces lender risk)

Typical approval time: 7-30 days

Repayment period: 90-365 days

Success factors:

- Property, vehicle, or equipment collateral worth ₦700,000+

- CAC-registered business with tax records and bank statements

- Government or corporate employment with verifiable ₦200,000+ salary

- Multiple guarantors (2-3 people) with strong credit

Lenders to approach:

- Established microfinance banks (Renmoney, AB Microfinance, LAPO)

- Bank of Industry for business loans

- Employer-partnered lenders for salary earmark

- Specialized asset-based lending institutions

Hard truth about ₦500,000: At this amount, most legitimate lenders will eventually want BVN even if you provide collateral, simply as additional verification layer. The few that truly don’t require it are relationship-based (credit unions where you’re a longstanding member, employers with strong internal verification, family/community lending networks).

Safer Alternatives to 100000 Naira Loan Without BVN

Before taking a risky path to get 100000 naira loan without BVN, 200000 naira, or 500000 naira loan without BVN, consider alternatives that might solve your problem without debt at all.

Government and NGO Grants

Multiple programs exist that give money (not loans) to Nigerians for specific purposes:

Tony Elumelu Foundation: ₦1 million grants for African entrepreneurs (highly competitive but no repayment required).

Bank of Industry (BOI) Development Finance Programs: Offers low-interest business loans and grants with flexible verification.

Youth Enterprise with Innovation in Nigeria (YouWiN): Government program offering business grants to young entrepreneurs.

Agricultural programs: NIRSAL, Anchor Borrowers Program, and others offer financing specifically for farmers and agribusinesses.

Education loans: NELFUND provides interest-free student loans with repayment only starting 2 years after NYSC.

These programs have application processes, but success means free money or extremely favorable terms compared to commercial loans.

Crowdfunding and Community Support

Nigerian crowdfunding platforms and community networks can raise substantial amounts:

GoFundMe Nigeria: For medical emergencies, education, disasters, you can raise ₦100,000-₦500,000 from sympathetic donors.

Nairaland forums: Community members sometimes pool resources for legitimate verified needs.

Religious organizations: Churches, mosques, and religious groups often have benevolence funds for members in crisis.

Professional associations: Many trade and professional groups offer financial assistance to members.

Family networks: Extended family pooling ₦20,000-₦50,000 each can raise ₦200,000-₦500,000 collectively.

Asset Liquidation

Sometimes the fastest path to ₦100,000-₦500,000 is selling what you already own:

Electronics: Laptops, phones, cameras, gaming consoles sell quickly on Jiji, Facebook Marketplace, Instagram.

Vehicles: Even older vehicles have value. Consider selling and using public transport temporarily.

Land or property: If you own land, selling a portion or the whole property might solve the problem permanently.

Business inventory: If you’re a trader, liquidating slow-moving stock generates immediate cash.

Valuables: Jewelry, watches, collectibles, antiques can be sold to collectors or specialized buyers.

Yes, selling assets hurts emotionally. But it’s infinitely better than taking a predatory loan at 50% monthly interest that leads to losing everything anyway.

Business Revenue Acceleration

If you need money for business, sometimes the answer is accelerating revenue rather than borrowing:

Advance payments: Offer 10-20% discounts to customers who pay upfront for future deliveries.

Flash sales: Deep discount sales generate quick cash flow (better than paying loan interest).

Partner investment: Bring in a partner who invests capital in exchange for equity share.

Invoice factoring: Sell your accounts receivable (money customers owe you) at a discount to get immediate cash.

Pre-selling: Sell products/services before you create them, use customer money to fund production.

For entrepreneurs exploring sustainable growth without crushing debt, understanding profitable business strategies helps more than any loan.

Red Flags and Warning Signs

As you explore options for large loans without BVN, watch for these danger signals:

Lender red flags:

- No physical office or verifiable business address

- Only contactable through WhatsApp, Telegram, or social media

- Not registered with CBN, FCCPC, or any regulatory body

- Website is poorly designed with spelling/grammar errors

- They contact you first (unsolicited loan offers via SMS/WhatsApp)

- Promise approval before seeing any of your information

- Request upfront fees before disbursement

Terms red flags:

- Interest rates above 30% monthly

- Unclear or constantly changing loan terms

- No written contract or agreement

- Repayment schedule that’s impossibly short

- Penalties that exceed the original loan amount

- Automatic access to your bank account

- Requirements to install unknown apps with excessive permissions

Behavioral red flags:

- Pressure to decide immediately

- Threats if you ask questions or request time to think

- Unwillingness to let you consult family/friends

- Demands for secrecy (“Don’t tell anyone about this opportunity”)

- Requests for unusual collateral (certificates, passports, BVN documents)

- Asking you to recruit others (pyramid scheme structure)

Collection practice red flags:

- Threats of violence or arrest before loan is even disbursed

- Demands for personal passwords or OTP codes

- Instructions to lie to your bank about transaction purposes

- Requirements to provide access to your contacts for “verification”

If you encounter any of these, walk away immediately. Legitimate financial difficulty is bad enough without adding scams and predatory lenders to the mix.

Building Your Financial Profile for Future Access

Rather than desperately seeking ₦500,000 without BVN today, invest time building financial credibility that makes larger loans accessible and affordable later.

Step 1: Get Your BVN (If You Don’t Have One)

I know this guide is about loans without BVN, but hear me out. If your BVN hesitation is about privacy concerns or inconvenience rather than legal issues, consider getting it. The long-term financial access benefits far outweigh the registration hassle.

Visit any bank branch with valid ID. Complete the BVN enrollment form. Get your fingerprints and photograph captured. Receive your BVN within 24-48 hours.

Having BVN opens access to better interest rates, larger loan amounts, formal banking services, and legitimate business opportunities.

Step 2: Build Credit History Strategically

Start with small, manageable loans. Repay perfectly on time or early every single time. Gradually increase loan amounts as your limits grow. Diversify across 2-3 reputable lenders (not 10+). Request credit reports periodically to track your progress.

Good credit history is wealth. It reduces interest rates, increases access, and gives you negotiating power with lenders.

Step 3: Document Everything

Maintain organized financial records:

- Bank statements showing transaction history

- Employment letters, payslips, contracts

- Business registration, tax clearance, licenses

- Property documents, vehicle papers, asset receipts

- Previous loan agreements and repayment records

When you approach lenders, comprehensive documentation dramatically improves approval odds and terms.

Step 4: Join Cooperative Societies

Cooperatives are underrated financial tools in Nigeria. Monthly contributions of ₦5,000-₦10,000 build:

- Savings that accumulate over time

- Access to low-interest cooperative loans

- Network of guarantors (fellow members)

- Financial discipline and planning skills

- Emergency support system

Many successful Nigerians credit cooperatives for their early financial stability.

Step 5: Develop Multiple Income Streams

The best protection against loan dependency is sufficient income. Consider:

- Freelancing or consulting in your skill area

- Small business alongside employment

- Online income through content creation, e-commerce

- Investment income from stocks, real estate, cryptocurrency (carefully)

- Rental income from property or equipment

Multiple income sources make you more attractive to lenders and reduce the need to borrow at all.

For practical ways to generate additional income, explore legitimate money-making apps and remote work opportunities that build sustainable financial stability.

Frequently Asked Questions

Large loans without BVN are extremely rare from legitimate sources. You’ll need alternative verification like NIN, collateral, guarantors, or salary earmark. Most no BVN claims for large amounts are scams.

Collateral is the most reliable alternative. Property, vehicles, or equipment worth ₦150,000-₦700,000+ can secure loans from microfinance banks without heavy BVN dependence, with lower interest rates at 5-15% monthly.

Approval takes 3-30 days depending on verification method. NIN verification needs 1-7 days, collateral assessment takes 7-14 days, guarantor verification requires 5-14 days, and business documentation needs 14-30 days.

Without BVN, expect 15-30% monthly interest for unsecured loans. Collateral-backed loans offer better rates at 5-15% monthly. BVN-verified loans charge just 3-10% monthly, showing the premium cost of avoiding verification.

No. WhatsApp offers promising large amounts without verification are almost always scams. Legitimate lenders have physical offices, websites, CBN or FCCPC registration, and never request upfront fees before disbursement.

Some lenders accept NIN for up to ₦100,000-₦200,000. QuickCheck, Carbon, and FairMoney consider NIN combined with strong transaction history. Above ₦200,000, most eventually require BVN for verification.

Acceptable collateral includes land titles, vehicle registration papers, business equipment, electronics, jewelry, and certificates of deposit. Lenders typically offer 50-70% of the collateral’s appraised value as loan amount.

Verify lender registration with CBN or FCCPC, never pay upfront fees, confirm physical office address, check online reviews, avoid WhatsApp-only lenders, and be suspicious of promises that sound too good to be true.

Key Takeaways: Making Smart Decisions

Let’s summarize the essential points for accessing ₦100,000 to ₦500,000 when BVN verification is challenging.

₦100,000-₦500,000 loans truly without BVN are extremely rare from legitimate sources. Most claims are scams, and the few real options involve significant trade-offs.

Alternative verification methods exist: NIN, collateral, guarantors, salary earmark, and business documentation can substitute for BVN in specific circumstances with legitimate lenders.

The hybrid strategy works best: Start with small BVN-free loans, build credit history, progressively access larger amounts, and strategically provide BVN only when you’ve built negotiating power.

Collateral offers the most reliable path to large amounts without BVN. If you have assets worth ₦150,000-₦700,000+, collateral-based loans from microfinance banks or credit unions provide legitimate ₦100,000-₦500,000 access.

Guarantor-based loans require strong relationships with people willing to stake their creditworthiness on your repayment. Family members or very close friends with good credit and verified income.

Salary earmark is ideal for employed people, offering ₦150,000-₦450,000 based on monthly income, with repayment automatically deducted from paycheck, reducing lender BVN dependency.

Business documentation opens doors for entrepreneurs with CAC registration, tax clearance, bank statements, and evidence of operations. Business-focused lenders assess company viability more than personal BVN.

Scams are everywhere: Any “instant ₦500,000, no BVN, no verification” offer is either fraudulent or predatory. Legitimate lending requires some form of credible verification.

Building financial credibility takes time but pays long-term dividends. Six months of strategic borrowing and repayment opens access to amounts and rates that desperate immediate borrowing never will.

Alternatives often beat loans: Government grants, crowdfunding, asset sales, revenue acceleration, or cooperative support might solve your ₦100,000-₦500,000 need without debt.

If you’re considering large loans for business purposes, also explore business loan options without BVN to understand sector-specific opportunities and requirements.

Remember: Legitimate lenders want to lend money (that’s how they profit), but they also need reasonable assurance of repayment. If you can’t provide BVN, you must provide something else of comparable value – collateral, guarantors, employment verification, or documented business operations.

The path to ₦100,000-₦500,000 without BVN exists, but it requires patience, strategy, and realistic expectations rather than chasing get-rich-quick schemes that end in financial disaster.

{kind=link}